SearchPulse Q2 Tells a Familiar Story

At the start of the year we began SearchPulse - surveying 2,000 respondents about their search behaviours, using a nationally representative age split. That survey showed that while Google was still king, there was plenty of change brewing, in particular around social search for specific intents.

For Q2, we asked a new set of respondents and our previous findings have been completely validated. In fact there was only a roughly +/4% variation between Q1 and Q2. Not only does this help to reinforce our insights from Q1, it also demonstrates that the much-talked-about impact of AI search might not be moving as fast as many fear.

This time, we dug deeper into the combined dataset of both reports to explore more around the choices and behaviours that are affecting Search.

Active vs. Passive Search Behaviour

While broadly speaking, traditional search engines are the dominant search tool, social media was a significant proportion of many respondents' search journeys, especially for particular search intents. The largest of these was ‘Looking for inspiration’, with 47% of respondents saying they use social media to perform these types of searches.

There’s a definite industry narrative surrounding younger generations’ search behaviours that social media is ‘taking over’, but that misses some of the crucial context. While inspiration might be a particular example of an intent where social media platforms have grown their presence, that’s not true for every intent.

It’s also important to highlight that there’s a fundamental difference between search behaviours that are ‘active’, such as Google or Bing searches, and those that are ‘passive’, such as social media platforms that surface algorithmically similar content to a user’s past interests. That said, some social platforms, like Pinterest, blur the lines by enabling more intentional, search-driven behaviours alongside passive browsing.

What remains to be seen is whether the introduction of AI mode and other AI features to the traditional Google search experience will introduce a more ‘passive’ experience for users who opt-in. Responses to the SearchPulse survey indicate that the greatest strength of Google is that it is “simple”, “quick” and “clear” - characteristics that Google is clearly leaning into, potentially at the expense of accuracy and nuance. This raises questions about how closely these developments align with Google’s original mission “to organise the world’s information and make it universally accessible and useful”

It’s a Search Journey - not a destination

The responses also highlighted a key factor in the modern search experience. While individual platforms might be preferred as the ‘first port of call’ for particular intents, the overlap and combination of tools used for a single search session are becoming increasingly blurred.

While many people default to Google for it’s ease of use - responses indicated that if Google couldn’t provide a clear answer, users would move to ask ChatGPT (the most popular AI search platform). In particular, respondents highlighted that AI search was their way of getting specific guidance that was tailored to their specific needs rather than the more general results that Google offered in the first instance.

This is particularly relevant due to the dominance of Search Engines when it comes to doing product research before purchases. As tools like ChatGPT and Perplexity introduce more and more unique tailoring to the specific user and their needs, as well as using data from Reddit and Quora - we might see that the need to jump between multiple tools becomes less impactful.

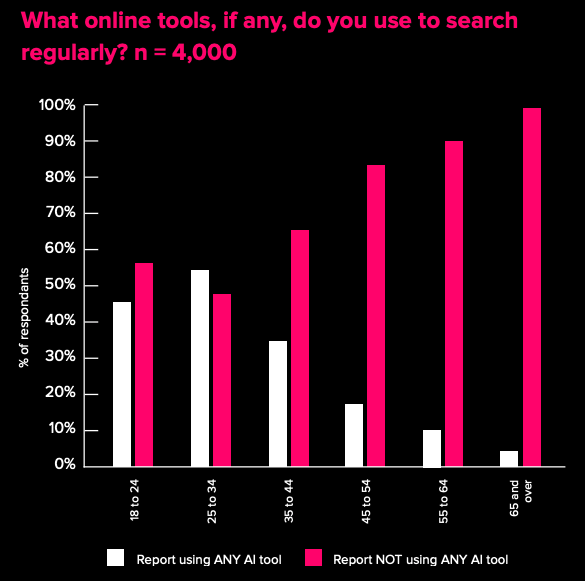

Change is stratified by age

There is likely no surprise in saying that the change in search behaviour is driven differently across age demographics. Younger age groups appear to use Google search less often than their older counterparts - but interestingly, the primary intent behind its use remains consistent (mainly informational).

There is a definite preference from younger people to use social media over traditional search engines, potentially driven by a preference for visually engaging content and community, but also potentially, the passive search experience appeals more to that demographic.

The key area of adoption change though, is between traditional and AI search tools. Regular AI usage peaks at the 25-34 age bracket, with a downward trend towards older groups. That has significant implications for optimisation or marketing efforts focused on those channels as it skews quite heavily towards the ‘early-adopters’.

There is a potentially significant driver of this adoption difference that we also uncovered - in that 19% of respondents used AI to search for work purposes. That was the second highest intention behind research purposes. That connection between work and AI usage not only helps to explain why younger generations might be more comfortable using it in general, it indicates that people who have been in their careers longer are potentially less likely to engage with the transformational potential of AI use at work.

Find more in our full SearchPulse Q2 2025 report

We couldn't possibly cover everything from the full report here. To truly understand the evolving landscape of search behaviour and delve deeper into our findings, visit the SearchPulse website. You can even interact with our AI agent to extract the most relevant insights for your needs.

If you want to discuss where AI sits in your strategy, get in touch with our team.

Contact Us

MEET THE AUTHOR.

MATT GREENWOOD-WILKINS

Matt is a data and spreadsheet nerd. Having worked in data pipeline engineering, business intelligence and data analysis - he helps us manage and understand data to generate interesting and actionable insights. He helps to drive efficiencies both internally and for clients, creating innovative solutions using automation, machine learning and AI.

More about Matt